400-700-9596

ACCAF2难点解析|考官文章分析

发表时间:2017-03-20 16:59

编辑:金程ACCA

告诉小伙伴:

3月ACCA考试已于上周结束了,不管这次ACCA考试考的怎么样,还是要打起精神继续迎接新6月的挑战。在进行3月份考试总结的同时,金程小编给大家准备了6月ACCA考试F2难点解析。

ACCAF2难点解析—UNDER OR OVER ABSORPTION

3月ACCA考试已于上周结束了,不管这次ACCA考试考的怎么样,还是要打起精神继续迎接新6月的挑战。在进行3月份考试总结的同时,金程小编给大家准备了6月ACCA考试F2难点解析。

在这篇文章中,主要介绍一下这个知识点—under or over absorption,并结合几道F2的考题的讲解,希望同学们可以掌握F2的这个难点。

Under or Over absorption

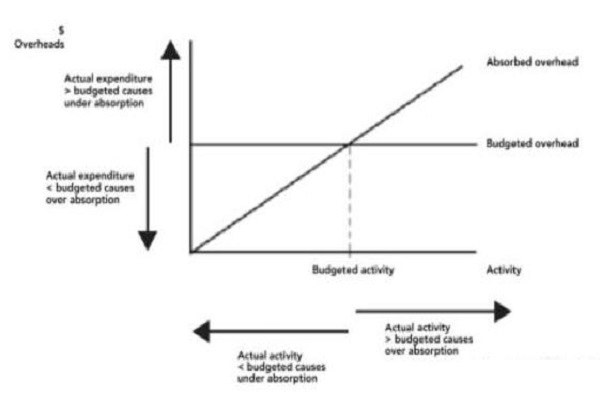

正如上图所示,under or over absorption can be caused by the following reasons

1 the difference between actual expenditure and budgeted expenditure

2 当actual expenditure大于budget expenditure时, 会产生under absorption

3 当actual expenditure 小于 budget expenditure时,会产生over absorption

4 The difference between actual activity and budgeted activity

5 当actual activity 大于budget activity时,会产生over absorption

6 当actual activity 小于budget activity时,会产生under absorption;

上面是关于under/over absorption的知识点的总结,其背后所包含的逻辑已经在考友论坛发表过啦,如果同学们对这一部分的知识感兴趣,可以自己翻阅查找哟!

Question practice

Question one:

The following question was identified as being badly answered in a previous F2 Examiner’s report.

A company uses absorption costing with a predetermined hourly fixed overhead absorption rate. Last year, the following situations arose:

1.Actual overhead expenditure was less than the budgeted expenditure.

2.Actual hours worked were less than the budgeted hours used to set the predetermined overhead absorption rate.

Which of the following statements is correct?

1.Both situations would cause the overheads to be under absorbed

2.Both situations would cause the overheads to be over absorbed

3.Situation (1) would cause the overheads to be under absorbed and situation (2) would cause the overhead to be over absorbed

4.Situation (1) would cause the overheads to be over absorbed and situation (2) would cause the overhead to be under absorbed

The correct answer is 4

答案解析:在考试中,很多考生都错误地选择了 answer 2, 也就是说,同学们对于situation (1)所产生的over absorbed是可以理解的,但是没有真正地理解situation (2). 在situation (2)下,由于actual hours 比 budget hours小,即:actual activity小于budget activity, 因此实际活动所吸收的overhead ( absorbed overhead)是小于budget overhead, 因此就产生了under absorbed.

Question two:

A company uses an overhead absorption rate of $3.50 per machine hour, based on 32,000 budgeted machine hours for the period. During the same period the actual total overhead expenditure amounted to $108,875 and 30,000 machine hours were recorded on actual production.

By how much was the total overhead under or over absorbed for the period?

A Under absorbed by $3,875

B Under absorbed by $7,000

C Over absorbed by $3,875

D Over absorbed by $7,000

The correct answer is A

通过这道题目,可以很好地让同学们掌握这个方面的知识。

Under/ over absorption is the difference between actual overhead and absorbed overhead based on actual activity level

根据上述定义,可以得到下面的公式

Under/ over absorption = absorbed overhead – actual overhead

1 如果absorbed overhead大于actual overhead, over absorbed

2 如果absorbed overhead小于actual overhead, under absorbed

根据上述公式,我们可以直接计算得到under absorbed by $3,875

下面,小编我将会把这个under absorption ($3,875)进行以下的分解。

1 第一部分:the difference between actual expenditure and budgeted expenditure

=budgeted expenditure – actual expenditure

=$3.5 * 32,000 - 108,875=$3,125 (over absorbed )

2 第二部分:The difference between actual activity and budgeted activity

= (32,000-30,000) * OAR= $7,000 (under absorbed)

因此,total amount is $ 3875 (under absorbed)

F2考官文章分析-marginal costing

In marginal costing, fixed production costs are treated as period cost(期间费用)written off as they are incurred;

In absorption costing, fixed production costs are absorbed into the cost of sales units and are carried forward in inventory to be charged against sales for the next period;

Marginal costing 与 absorption costing 本质区别的来源:产量

?在marginal costing下,all incurred fixed overhead直接当作期间费用扣除;(according to 当期产量 production units )

?而相对地,在absorption costing下,fixed overhead可以作为cost of sales 扣除;(according to 当期销量 sales units )

因此,marginal costing 与 absorption costing之间的差异体现在以下几个方面:

第一,期末利润的不同=(产量-销量)* overhead absorption rate per units

第二,期末存货价值的不同= the change in inventory level * overhead absorption rate per units

同时,有关于inventory的相关公式:

The closing inventory = the opening inventory + production units – sales units

公式变形为:

The change in inventory level = the closing inventory – opening inventory

= production units (产量) – sales units (销量)

结合上面所总结的知识,我们得出下面的相关结论:

Difference in profits = change in inventory level * overhead absorption rate per unit

1. If closing inventory opening inventory, then absorption costing profit will be greater than marginal costing profit;

2. If opening inventory closing inventory, then absorption costing profit will be less than marginal costing profit;

Question practice

A company which uses marginal costing has a profit of $37,500 for a period. Opening inventory was 100 units and closing inventory was 350 units. The fixed production overhead absorption rate is $4 per unit.

What is the profit under absorption costing?

A $5,700

B $5,500

C $8,500

D $9,300

The correct answer is C

根据上面所总结的规律,我们可以知道:

The change in inventory level = 350-100= 250 units

Different in profits = the change in inventory level * overhead absorption rate

= 250 units * $4 per units= $1,000

The profit under absorption costing= profit under marginal costing + different in profits= $37,500 + $1,000 = $38,500

填写资料领取ACCA考试资料

课程

课程 题库

题库 直播

直播 代报名

代报名 微信

微信

资料索取

资料索取  代理报名

代理报名  课程咨询

课程咨询  400-700-9596

400-700-9596